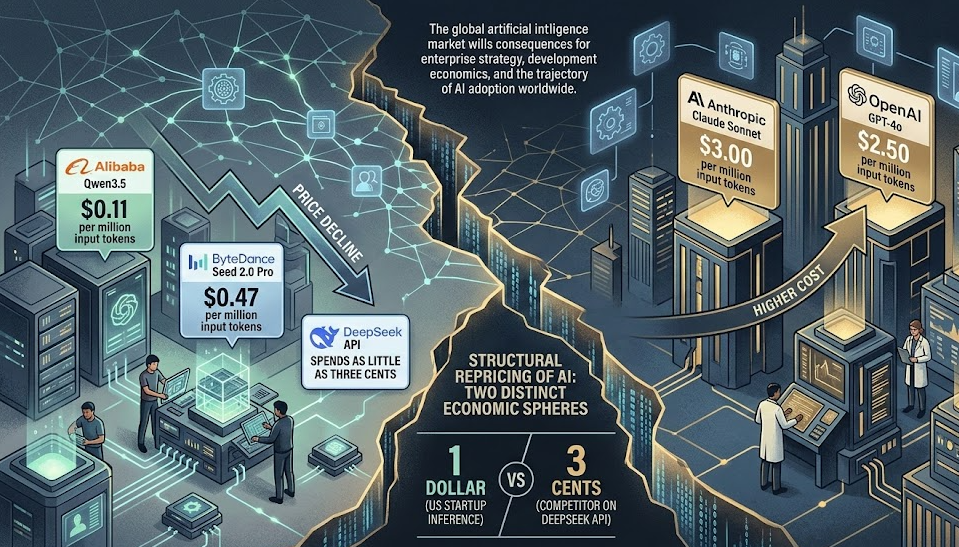

Chinese AI labs are now selling frontier-class intelligence at one-tenth the price of American rivals, and the gap is widening. In February 2026, Alibaba launched Qwen3.5 at roughly $0.11 per million input tokens while ByteDance's Seed 2.0 Pro debuted at $0.47. Compare that to Anthropic's Claude Sonnet at $3.00 or OpenAI's GPT-4o at $2.50, and the arithmetic is stark: for every dollar an American startup spends on inference, a competitor using DeepSeek's API spends as little as three cents.

This is not a rounding error. It is a structural repricing of artificial intelligence that is cleaving the global market into two distinct economic spheres—with profound consequences for enterprise strategy, development economics, and the trajectory of AI adoption worldwide.

The Pricing Chasm: A Quantitative View

The scale of the cost differential defies easy explanation by efficiency gains alone. DeepSeek's V3.2 model charges $0.07 per million input tokens on cache hits—roughly 30x cheaper than Claude Sonnet and 25x below GPT-4o. Alibaba's Qwen3.5-Plus, a 397-billion-parameter mixture-of-experts model activating only 17 billion parameters per token (~5% activation), prices input at approximately $0.11.

Comparative Pricing Matrix

| Provider / Model | Input (per 1M tokens) | Output (per 1M tokens) | Origin | Tier |

|---|---|---|---|---|

| DeepSeek V3.2 (cached) | $0.07 | $0.28 | China | Budget |

| Alibaba Qwen3.5-Plus | $0.11 | N/A | China | Budget |

| MiniMax M2.5 | $0.20–$0.30 | Varies | China | Mid |

| ByteDance Seed 2.0 Pro | $0.47 | $2.37 | China | Mid |

| Google Gemini 2.5 Flash | $0.30 | Varies | US | Mid |

| OpenAI GPT-4o | $2.50 | $10.00 | US | Frontier |

| Anthropic Claude Sonnet | $3.00 | $15.00 | US | Frontier |

| Anthropic Claude Opus 4.5 | $5.00 | $25.00 | US | Frontier+ |

| OpenAI GPT-5.2 | $1.75 | $14.00 | US | Frontier |

Mechanisms Sustaining the Price Gap

- Massive subsidies: Alibaba's $400M coupon campaign drove Qwen daily active users from 7M to 58M in a single week.

- Government support: Local governments distribute computing power vouchers subsidizing inference costs.

- State-linked VC: Approximately $184 billion channeled to ~10,000 AI firms over the past decade (per Stanford research), underwriting losses no purely commercial entity could absorb.

- Open-source as acquisition: MIT/Apache 2.0 licensing for nearly every major Chinese model functions as a developer acquisition channel, monetized through cloud platform lock-in.

- Architectural efficiency: Qwen3.5's sparse MoE architecture activates fewer than 5% of parameters per inference, dramatically reducing compute overhead.

Benchmark Convergence: Performance No Longer Justifies the Premium

Price discounts matter only if performance follows. It now does. ByteDance's Seed 2.0 Pro scored 98.3 on AIME 2025 (surpassing GPT-5.2's 93) and 3,020 on Codeforces, approaching grandmaster territory. MiniMax's M2.5 achieved 80.2% on SWE-bench Verified, edging past GPT-5.2's 80.0% and trailing Claude Opus 4.6's 80.8% by a fraction. Alibaba claims Qwen3.5 outperforms GPT-5.2 and Claude Opus 4.5 on 80% of evaluated benchmarks.

Third-party leaderboard data shows Chinese models occupying 14 of the global top 20 positions on OpenCompass rankings across reasoning, coding, and mathematics. The capability gap that once justified premium pricing has compressed to single-digit percentage differences on most standardized measures.

Selected Benchmark Comparisons

| Benchmark | Seed 2.0 Pro | MiniMax M2.5 | GPT-5.2 | Claude Opus 4.6 |

|---|---|---|---|---|

| AIME 2025 | 98.3 | — | 93.0 | — |

| Codeforces Rating | 3,020 | — | — | — |

| SWE-bench Verified | — | 80.2% | 80.0% | 80.8% |

| τ²-Bench (Tool Use) | 90.4% | — | — | — |

The Agentic Frontier

The agentic frontier is equally contested. Anthropic pioneered computer use, the Model Context Protocol (now an open standard under the Linux Foundation), and Claude Code for autonomous software development. OpenAI ships Operator, Codex, and a full Agents SDK.

Chinese labs have responded with equivalent capabilities: Qwen Code CLI mirrors Claude Code; ByteDance's TRAE provides an AI-native coding IDE; Seed 2.0 Pro scores 90.4% on τ²-Bench for tool-calling autonomy; and Kimi K2.5 executes 200–300 sequential tool calls without human intervention. Both Qwen3.5 and Doubao 2.0 emphasize the ability to execute multi-step, real-world tasks autonomously—interpreting screen interfaces, coordinating cross-application workflows, and transforming hand-drawn sketches into functional code.

The Trust Premium: Why Enterprises Pay 10x More

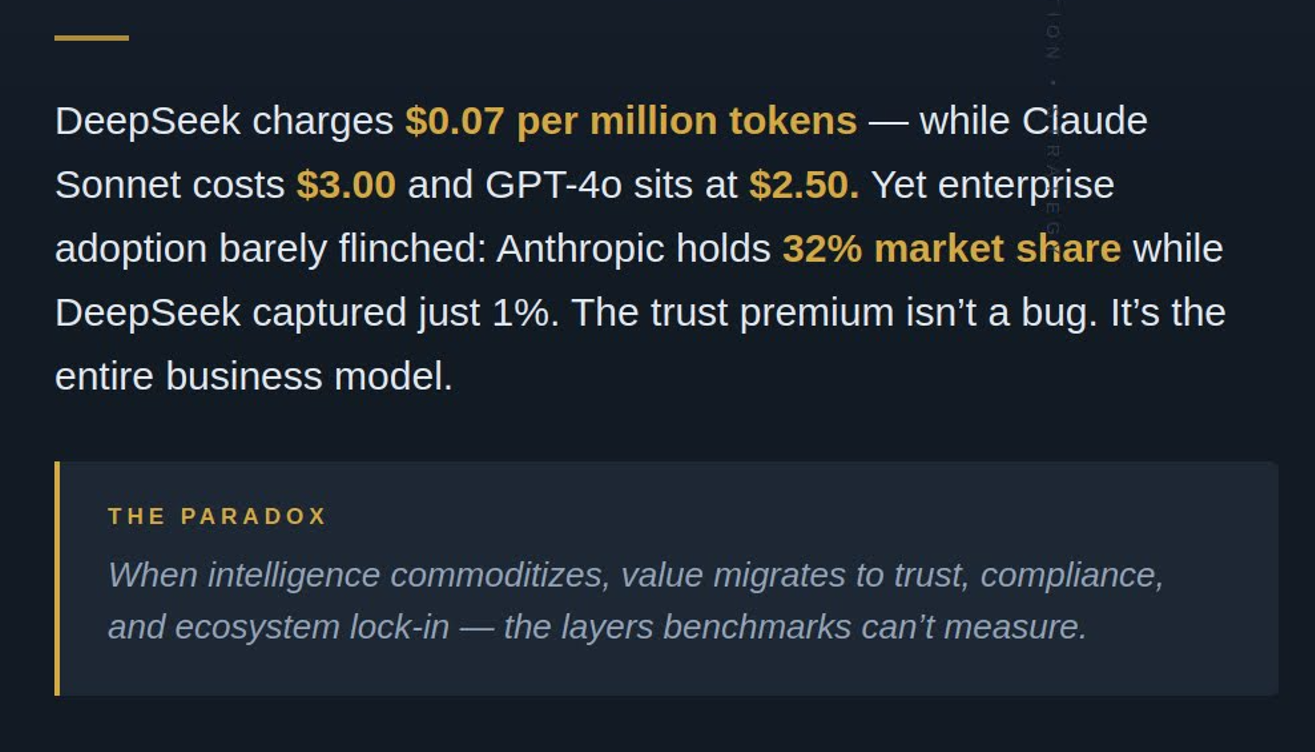

Despite converging performance, enterprise adoption tells a radically different story. Menlo Ventures' 2025 survey of 495 enterprise AI decision-makers found Anthropic commanding 32% market share, OpenAI 25%, and Google 20%. DeepSeek captured just 1%.

The explanation is not technical—it is legal, regulatory, and structural.

Regulatory and Security Barriers

- China's National Intelligence Law requires all organizations to "support, cooperate with, and collaborate in national intelligence work."

- DeepSeek's privacy policy states all data resides on PRC servers with no alternative routing.

- The US DOJ Bulk Data Transfer Rule (effective April 2025) makes sending sensitive data to Chinese-jurisdiction servers a potential criminal offense—fines up to $1M and 20 years imprisonment.

- Security researchers at Wiz discovered an unsecured DeepSeek database exposing over 1 million chat logs.

- NowSecure found hard-coded encryption keys and unencrypted data transmission in DeepSeek's iOS app.

- Cisco testing recorded a 0% harmful prompt block rate for DeepSeek.

Government Bans and Restrictions

NASA, the Pentagon, and the US Navy ban DeepSeek outright. Texas, New York, and Virginia prohibit it on state devices. Italy ordered its removal from app stores. Australia banned it from all government systems. Bipartisan congressional bills would extend restrictions to federal contractors.

For any enterprise serving government clients or handling regulated data—finance, healthcare, defense, critical infrastructure—the compliance risk alone renders Chinese models unusable regardless of price.

Two Markets, Two Logics: The Bifurcated Global Landscape

What emerges is not a single global AI market but a bifurcated one, segmented less by capability than by regulatory jurisdiction and risk tolerance.

Market Segmentation by Adoption

| Segment | Likely Preference | Economic Rationale |

|---|---|---|

| Western Multinationals | US models (Claude, GPT) | Risk aversion and regulatory alignment outweigh cost savings |

| Emerging Market Enterprises | Hybrid approach | Cost sensitivity balanced against local data regulations |

| Global Startups & SMBs | Chinese models (Qwen, etc.) | Price elasticity dominates; limited compliance overhead |

| Developing Economies | Chinese models | AI becomes economically viable for the first time at these price points |

RAND Corporation analysis across 135 countries found Chinese models exceeding 20% market share in 11 nations, with strongest adoption in developing economies and countries with close political ties to Beijing. More than half of DeepSeek's users are in China, India, and Indonesia.

Classical Bertrand price competition theory predicts that in markets with near-homogeneous products, the lowest-price firm captures all demand. The AI market deviates for three reasons: substantial switching costs and ecosystem lock-in (Menlo found 90% of firms concentrate on a single provider), regulatory barriers functioning as non-tariff trade walls, and trust operating as a quality dimension that benchmarks cannot capture.

The Jevons Paradox: Cheaper Intelligence Unleashes Demand

Over 2025, the cost to achieve a given AI benchmark score plunged from $4,500 per task to $11.64—a 99.7% reduction. Yet OpenAI's inference spending tripled to $7 billion. Enterprise LLM API spending doubled from $3.5B to $8.4B in six months. Cheaper intelligence does not reduce demand; it unleashes it.

Chinese pricing pressure expands the total addressable market rather than merely redistributing share, which explains why Anthropic's revenue run rate grew from $1 billion to $9 billion in roughly twelve months even as competitors offered comparable capabilities at a fraction of the price. The AI API market is projected to reach $179 billion by 2030.

Where Value Migrates When Models Commoditize

Foundation models are following the trajectory of semiconductors, cloud compute, and bandwidth before them: performance converges, margins compress, and durable value migrates to adjacent layers.

- Nvidia captures 83% of generative AI revenue with margins above 88%.

- Cloud hyperscalers (AWS, Azure, Google Cloud) grew 26–48% YoY through the price war, collecting rent regardless of which model wins.

- Application-layer startups earned roughly $2 for every $1 captured by incumbents in 2025.

For US frontier labs, the strategic imperative is clear: compete on trust, compliance, and agentic ecosystem depth rather than unit token cost. Anthropic's MCP standard (now adopted by OpenAI and Google) creates switching costs through tooling integration. OpenAI's enterprise contracts embed security guarantees and audit rights that no Chinese provider can match under current law.

Companies that successfully leverage low-cost Chinese models for appropriate use cases may achieve superior margins, while firms overly dependent on premium Western APIs could face margin pressure as alternatives mature. The winners will be those who build abstraction layers enabling flexible model switching as the competitive landscape evolves.

Strategic Implications for Stakeholders

Enterprise Leaders

- Conduct granular risk-benefit analysis of model selection by use case.

- Pilot Chinese models for low-risk, high-volume tasks (content generation, customer support) while maintaining Western providers for sensitive workflows (financial analysis, healthcare, legal).

- Develop abstraction layers in AI architecture to enable flexible model switching.

- Recognize that 90% of firms concentrate on a single provider—plan switching costs accordingly.

Policymakers

Price competition alone will not determine AI leadership. Investment in domestic compute infrastructure and talent pipelines ensures strategic autonomy. Reciprocal data governance frameworks that enable secure cross-border AI collaboration without compromising national security should be considered. The divergence of regulatory regimes risks cementing separate AI ecosystems and reducing global knowledge spillovers.

Investors

Monitor the unit economics of AI deployment closely. Cost competition may redirect R&D investment toward efficiency breakthroughs rather than pure capability expansion. The application layer, tooling integration, and infrastructure plays (cloud, chips) may offer more durable returns than backing individual model providers in what is becoming an increasingly commoditized market.

Conclusion

The question is no longer whether AI becomes a commodity. It is whether the world can sustain two parallel commodity markets, governed by different rules, serving different masters, and running on increasingly divergent infrastructure—without the fracture lines becoming permanent.

The era of AI as a premium-priced novelty is ending. The era of AI as a scalable, economically transformative utility has begun. For enterprises navigating this landscape, the strategic calculus involves balancing capability convergence against trust premiums, cost optimization against compliance risk, and short-term savings against long-term ecosystem lock-in.

Disclaimer: This analysis is based on publicly available information as of February 2026. AI model capabilities and pricing evolve rapidly; readers should verify current specifications before making strategic decisions.