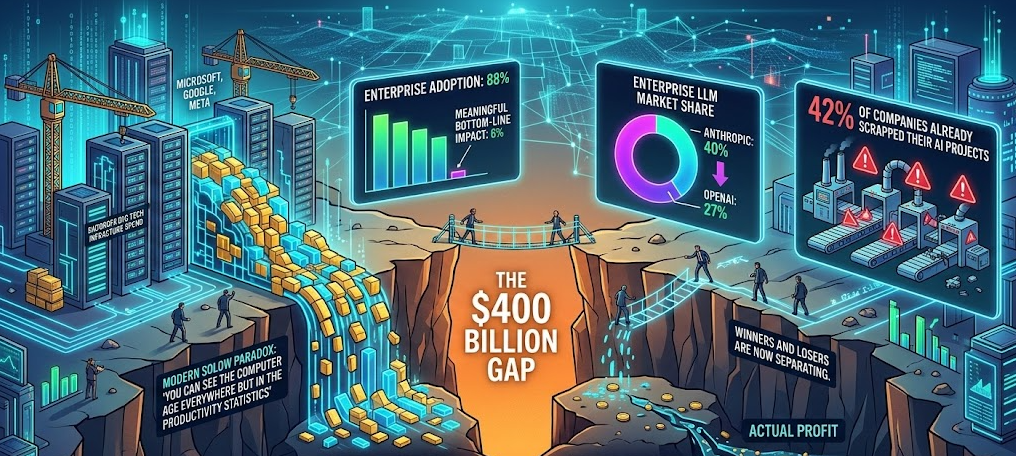

Artificial intelligence is generating staggering revenue growth and even more staggering losses. The emerging AI economy sits at a peculiar inflection point: enterprise adoption has reached 88% of organizations globally, yet only 6% report meaningful bottom-line impact. The data tells a clear story: Anthropic has captured 40% of enterprise LLM market share while OpenAI's share fell to 27%, Big Tech's $427 billion infrastructure spend dwarfs the $37 billion in actual enterprise AI revenue, and 42% of companies have already scrapped their AI projects. Somewhere between those investment figures and revenue figures lies the defining economic tension of 2026 — a modern instantiation of Robert Solow's famous paradox that "you can see the computer age everywhere but in the productivity statistics." The winners and losers are now separating, and the results are surprising almost everyone.

Anthropic vs. OpenAI: Who's Winning Enterprise AI in 2026?

The most consequential shift in the AI industry's brief history is playing out in enterprise boardrooms. Anthropic, the safety-focused lab founded by former OpenAI researchers, has seized 40% of enterprise LLM market share as of December 2025, according to Menlo Ventures — up from just 12% in 2023. OpenAI's share collapsed in the opposite direction, falling from a dominant 50% to roughly 27% over the same period.

The numbers tell a striking story. Anthropic reached $14 billion in annualized revenue by February 2026, with 80% flowing from enterprise customers. Its Claude Code product alone generates $2.5 billion in annual run-rate revenue. Eight of the Fortune 10 are Claude customers. Landmark deployments — Deloitte's rollout to 470,000 employees, Cognizant's 350,000-person deployment, a $200 million Snowflake partnership — reflect a company that has cracked enterprise distribution with remarkable speed.

OpenAI, by contrast, remains a consumer-first business. Its $20 billion ARR dwarfs Anthropic's topline, but only 25–30% derives from enterprise, with consumer subscriptions and ChatGPT's 900 million weekly users doing the heavy lifting. CFO Sarah Friar flagged enterprise as a "key focus" for 2026, and the company appointed Barret Zoph to lead an enterprise sales offensive in January. But OpenAI's gross margins are declining — from 40% to 33% — while Anthropic's trajectory runs the other direction. The enterprise AI race increasingly resembles Schumpeter's creative destruction: the incumbent's consumer dominance may prove a strategic liability as the market's center of gravity shifts toward business buyers demanding reliability, compliance, and measurable ROI.

The AI Revenue Gap: $427B in Spending, $37B in Returns

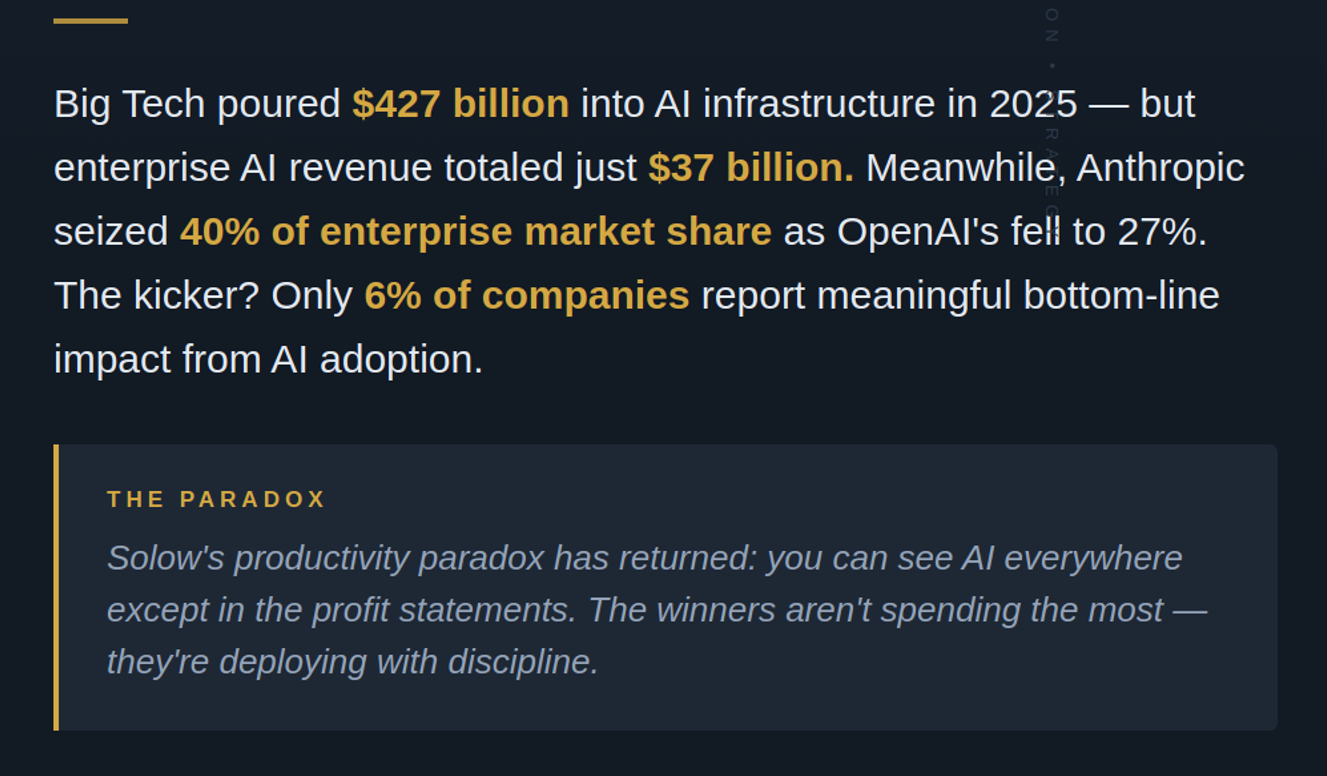

The gulf between AI investment and AI returns remains the industry's central economic problem. Big Tech committed approximately $427 billion in capital expenditure in 2025, with Google alone planning $175–185 billion for 2026. Meanwhile, total enterprise generative AI spending reached just $37 billion — a roughly 10:1 ratio of infrastructure investment to downstream revenue. Sparkline Capital's analysis, cited by Morningstar, calculates that AI revenues must increase 100-fold to $2 trillion annually by 2030 to justify current spending levels.

At the firm level, the picture is equally sobering. McKinsey's 2025 global survey found that only 39% of organizations attribute any EBIT impact to AI, and most of those estimate the impact at less than 5% of earnings. An S&P Global study revealed that 42% of companies scrapped most of their AI initiatives in 2025, up from 17% a year earlier. MIT research found 95% of enterprise AI projects failed to show measurable financial returns within six months.

This is not to say value doesn't exist — it does, but it concentrates sharply. BCG's AI leadership study found that AI leaders achieved 1.7 times the revenue growth and 3.6 times the total shareholder return of laggards. The gap between AI's winners and its experimenters is widening, not narrowing, and companies without formal AI strategies succeed at less than half the rate of those with them.

Consumer AI Monetization: Why ChatGPT Turned to Advertising

OpenAI's January 2026 announcement that it would begin testing advertisements in ChatGPT's free tier marked an inevitable pivot. With 95% of ChatGPT's users generating zero direct revenue and inference costs running into billions annually, the ad-supported model represents economic necessity dressed as strategic evolution. Mercedes-Benz, JPMorgan Chase, and Estée Lauder are among early advertisers. Internal models project $1 billion in ad revenue for 2026, with Evercore ISI forecasting the figure could exceed $25 billion by 2030.

The unit economics are punishing. ChatGPT consumes an estimated 17.2 billion kilowatt-hours annually, costing roughly $2.4 billion in electricity alone — approximately ten times the energy cost per query of traditional search. Sam Altman has admitted even the $200-per-month Pro plan can be unprofitable for power users. Google plans Gemini app advertisements for 2026, while Perplexity AI abandoned its ad strategy entirely, concluding that advertising corrodes the trust an "answer engine" requires. The consumer AI monetization question remains unresolved, and the Gartner Hype Cycle's trough of disillusionment looms for models that cannot demonstrate sustainable economics.

AI and Jobs: Augmentation Beats Replacement, But Most Companies Can't Tell

The labor economics data increasingly supports a nuanced conclusion: AI augments skilled workers and compresses skill gaps rather than eliminating jobs wholesale. A landmark Stanford study of 5,172 customer support agents found a 15% average productivity gain, with bottom-quintile workers experiencing a 36% improvement — powerful evidence for the "skill compression" thesis. Georgia State University's analysis of five million U.S. patents found that generative AI technologies drove more hiring, greater productivity, and higher firm value in augmented occupations.

Yet the aggregate picture remains paradoxically flat. An NBER study of 6,000 executives found nearly 90% of firms reported zero measurable impact on employment or productivity over three years. U.S. productivity grew 2.7% in 2025 — nearly double the decade's average — but Erik Brynjolfsson's "J-curve" framework suggests we are only now exiting the investment phase where complementary reorganization masks technology's true impact. The critical danger is ego-driven adoption: deploying AI for appearances rather than returns. When 42% of C-suite executives report AI adoption is "tearing their company apart," the imperative shifts from implementation speed to implementation discipline — matching tools to workflows where measurable ROI exists.

Private AI Valuations: $1 Trillion in Wealth Retail Investors Can't Access

Perhaps the most underappreciated structural feature of the AI boom is its near-total concentration in private markets. Anthropic is valued at $380 billion, OpenAI at roughly $730 billion, and xAI at $200–245 billion — yet none trade publicly. Private AI venture investment reached $202–259 billion in 2025, representing over half of all global venture capital. Retail investors have virtually no direct access to these companies; the KraneShares AGIX ETF, one of the few vehicles offering private AI exposure, remains capped at 15% private holdings by SEC rules.

The implications are significant. Ten unprofitable AI startups added nearly $1 trillion in combined valuation through private rounds in the past year — wealth creation invisible to most investors. The circular financing structures raise additional concerns: Nvidia invests in OpenAI, which spends the capital on Nvidia GPUs; Microsoft invests in Anthropic, which commits billions to Azure. An IPO pipeline is forming — Databricks filed confidentially in January, and both OpenAI and Anthropic have engaged IPO counsel — but until these listings materialize, the AI economy's most explosive growth remains gated behind accredited-investor thresholds, concentrating transformative wealth among the already wealthy.

What This Means for Businesses and Investors

The AI economy in 2026 demands clear-eyed pragmatism. Anthropic's enterprise surge and OpenAI's consumer-to-enterprise pivot illustrate that the market is repricing around measurable business value, not benchmarks. The 10:1 ratio of infrastructure investment to enterprise revenue is historically unprecedented and structurally unsustainable without dramatic adoption acceleration. For businesses, the evidence is unambiguous: formal AI strategy correlates with double the success rate, and augmentation — not replacement — drives the strongest returns. For investors, the concentration of AI value creation in private markets represents both a generational opportunity locked behind institutional gates and a risk vector reminiscent of pre-2000 venture excess. The Solow Paradox resolved itself eventually for computing; the question for AI is whether patience or prudence will prove the wiser counsel.

Frequently Asked Questions

What percentage of enterprise AI market share does Anthropic have in 2026?

Anthropic captured 40% of enterprise LLM market share as of December 2025, according to Menlo Ventures' annual State of Generative AI report. This represents a dramatic increase from just 12% in 2023, driven primarily by enterprise adoption of Claude Code and large-scale deployments at Fortune 10 companies.

How much did Big Tech spend on AI infrastructure in 2025?

Big Tech companies collectively committed approximately $427 billion in AI-related capital expenditure during 2025. Google alone plans $175–185 billion for 2026. Meanwhile, total enterprise generative AI spending reached just $37 billion, creating a roughly 10:1 ratio of infrastructure investment to downstream revenue.

Is OpenAI or Anthropic more focused on enterprise customers?

Anthropic derives approximately 80% of its $14 billion ARR from enterprise customers, making it decisively enterprise-focused. OpenAI's $20 billion in revenue is larger overall, but only 25–30% comes from enterprise, with consumer subscriptions and ChatGPT's 900 million weekly users generating the majority. OpenAI's CFO Sarah Friar has publicly identified enterprise as a "key focus" for 2026.

Can retail investors invest in Anthropic or OpenAI?

Neither Anthropic nor OpenAI trades publicly. Retail investors have limited options: the KraneShares AGIX ETF provides indirect exposure but is capped at 15% private holdings by SEC rules. An IPO pipeline is forming — Databricks filed confidentially in January 2026, and both OpenAI and Anthropic have engaged IPO counsel — but direct public access remains unavailable.

Sources: Menlo Ventures 2025 State of Generative AI, McKinsey State of AI 2025, BCG AI Leadership Study, Stanford Productivity Research (NBER), Georgia State University Labor Market Analysis, S&P Global Enterprise AI Survey, Sacra Revenue Data, Bloomberg/CNBC Valuation Reporting, Fortune CEO Survey 2025.