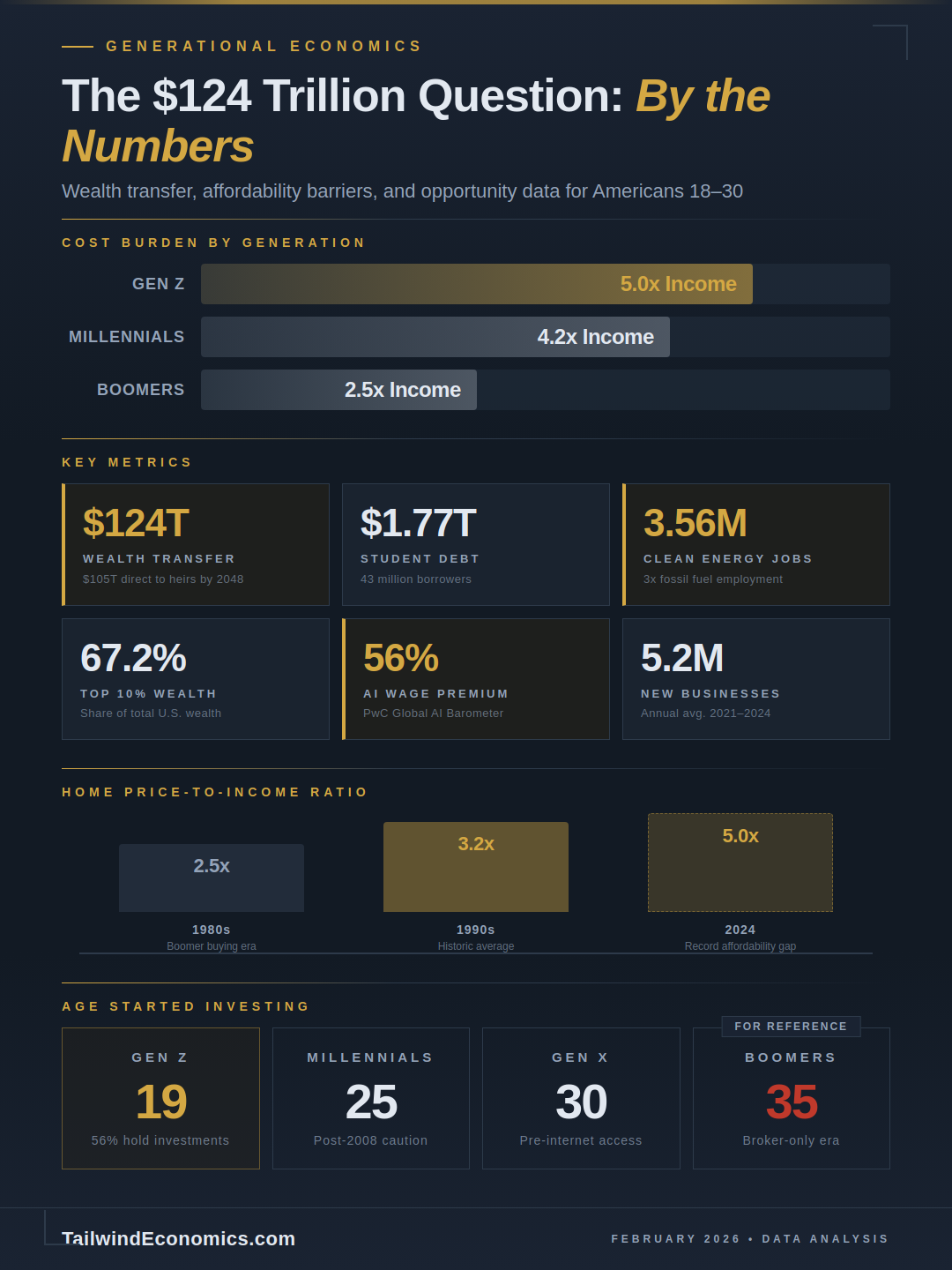

The largest inter-generational wealth transfer in human history is underway — and it will collide with a generation facing economic barriers their parents never encountered. Cerulli Associates revised its estimate sharply upward in 2024: $124 trillion in total wealth will change hands by 2048, with $105 trillion flowing directly to heirs. For Americans aged 18 to 30, this transfer represents both an unprecedented opportunity and a deepening fault line — because who inherits, what they inherit into, and which economic forces shape the decades ahead will determine whether this generation builds durable prosperity or watches it concentrate further.

A structural affordability crisis has redefined young adulthood

The traditional wealth-building playbook — earn a degree, buy a home, accumulate equity — has fractured under the weight of compounding cost pressures. The national home price-to-income ratio hit 5.0x in 2024, up from 3.2x throughout the 1990s, and the median age of a first-time homebuyer reached a record 38 years old, nearly a decade later than in 1981. Only 21% of home purchases in 2025 were made by first-time buyers, the lowest share since tracking began. Meanwhile, $1.77 trillion in outstanding student loan debt weighs on 43 million borrowers, with 20% behind on payments as of late 2024. Every $1,000 increase in student debt correlates with a 1.8% decline in homeownership among adults under 35.

Thomas Piketty's foundational insight — that when returns on capital exceed economic growth (r > g), wealth inequality widens structurally — frames this moment with uncomfortable precision. The top 10% of U.S. households now hold 67.2% of total wealth. The Great Wealth Transfer will not correct this imbalance; it will amplify it. More than half of the $124 trillion originates from just the top 2% of households, and white families remain nearly four times more likely to receive an inheritance than Black families. The Urban Institute concluded bluntly that this transfer "is poised to widen" the racial wealth gap, not close it.

Climate change is rewriting the economic map

A child born in 2024 faces an estimated $500,000 to $1 million in lifetime climate costs under high-emissions scenarios, according to an ICF study commissioned by Consumer Reports. These costs manifest through rising insurance premiums — up 49% since 2019 nationally, with Florida homeowners now paying an average $14,140 annually — as well as through depressed property values in vulnerable regions, climate-driven migration, and escalating disaster recovery expenses. NOAA recorded 27 billion-dollar weather events in 2024 alone, totaling $182.7 billion in damages.

Yet Schumpeter's framework of creative destruction suggests that disruption of this magnitude simultaneously creates extraordinary opportunity. The U.S. clean energy sector now employs 3.56 million workers — outnumbering fossil fuel workers three to one — and added nearly 100,000 jobs in 2024, growing at three times the rate of overall employment. The Inflation Reduction Act catalyzed over $450 billion in announced clean energy investments, and the ILO projects that the global green transition could create 8.4 million jobs specifically for young people by 2030. A critical green skills gap — demand surging 40% since 2015 while only 13% of the workforce is equipped — creates a structural hiring advantage for those who invest in the right capabilities now.

Young people are rewriting the investment playbook

Behavioral economics reveals a generation approaching capital markets with a fundamentally different psychology than their predecessors. Gen Z began investing at an average age of 19, compared to 35 for Baby Boomers. Fifty-six percent of Americans aged 18 to 25 now hold investments, with cryptocurrency serving as the entry point for 44% of them. The median Gen Z portfolio sits at $4,000 — modest in absolute terms, but the compounding runway ahead is vast.

This generation is also channeling economic anxiety into entrepreneurship at historic rates. Babson College's Global Entrepreneurship Monitor found that 24% of 18-to-24-year-olds are currently entrepreneurs, the highest rate of any age group for two consecutive years. Census Bureau data confirms the trend structurally: an average of 5.2 million new business applications were filed annually from 2021 to 2024, shattering previous records. The AI economy amplifies this entrepreneurial energy — workers with AI skills command a 56% wage premium, and generative AI job postings grew 50% between 2022 and 2024.

Positioning for the convergence ahead

The economic forces bearing down on young Americans are not random headwinds. They are structural shifts demanding strategic responses rooted in human capital theory and geographic flexibility. Clean energy and AI represent the twin engines of Schumpeterian creative destruction, and workers who build expertise at their intersection will command the highest premiums in the labor market through 2030 and beyond. Geographic arbitrage — leveraging remote work to capture Midwest and Southeast cost-of-living differentials — can accelerate wealth building by tens of thousands of dollars annually. Tax-advantaged accounts like Roth IRAs exploit the mathematical certainty that low current tax brackets and decades of compounding favor early, consistent investment.

The policy landscape matters too. Social Security's trust fund faces depletion by 2033, after which only 77% of benefits would be payable. Estate tax exemptions were permanently raised to $15 million per individual in 2025, further reducing checks on dynastic wealth concentration. These decisions shape the structural environment in which young people will build — or fail to build — financial security.

The $124 trillion transfer will reshape American wealth over the next two decades. But the more consequential story is whether a generation armed with unprecedented access to markets, positioned at the frontier of two simultaneous technological revolutions, and motivated by economic necessity can build wealth through productivity and strategic positioning rather than inheritance alone. The data suggest they are already trying. Whether the structure of the economy lets them succeed is the defining economic question of the next decade.