Artificial intelligence has triggered the most severe valuation collapse in software history. Public SaaS multiples have cratered 65–75% from their 2021 peaks, with median EV/Revenue ratios falling from 18–21x to roughly 5–7x by early 2026. More than $1 trillion in software market capitalization was destroyed in the weeks following Anthropic's Claude Cowork launch on February 3, 2026 Context Studios — an event Wall Street traders dubbed the "SaaSpocalypse." Ai2 +2 This isn't merely a rate-driven correction; it represents a structural reassessment of whether traditional software business models can survive in an era where AI commoditizes code, erodes per-seat pricing, and enables non-developers to build their own tools. Yet total software spending continues to grow — Gartner projects 14.7% growth to $1.4 trillion in 2026 SaaStrFinancialContent — revealing a market defined not by uniform destruction but by radical bifurcation between winners and losers.

From 21x to 5x: the anatomy of a multiple collapse

The compression in SaaS valuations is historically unprecedented in both scale and speed. According to the Meritech Capital Software Pulse, the median next-twelve-months revenue multiple for public SaaS peaked at 21.3x in late 2021 and stood at just 6.3x by March 2024 — a 71% decline. The 90th percentile fell even harder, from 52.3x to 13.7x, a 74% drop. Meritechcapital By December 2025, the Aventis Advisors SaaS Index placed the median at 5.1x EV/Revenue, reflecting a 73% decline from the 2021 peak. Aventis

The BVP Cloud Index (EMCLOUD) — the industry's benchmark for cloud software — tells a consistent story. Its median forward revenue multiple fell from approximately 18.4x at peak to 6.3x in Q1 2025. The private markets mirrored this trend with a lag: the Bessemer Cloud 100 average revenue multiple declined from 34x in 2021 to 20x in 2025, a 41% compression, Bessemer Venture Partners though the top private companies still command premiums over their public peers. Bessemer Venture Partners

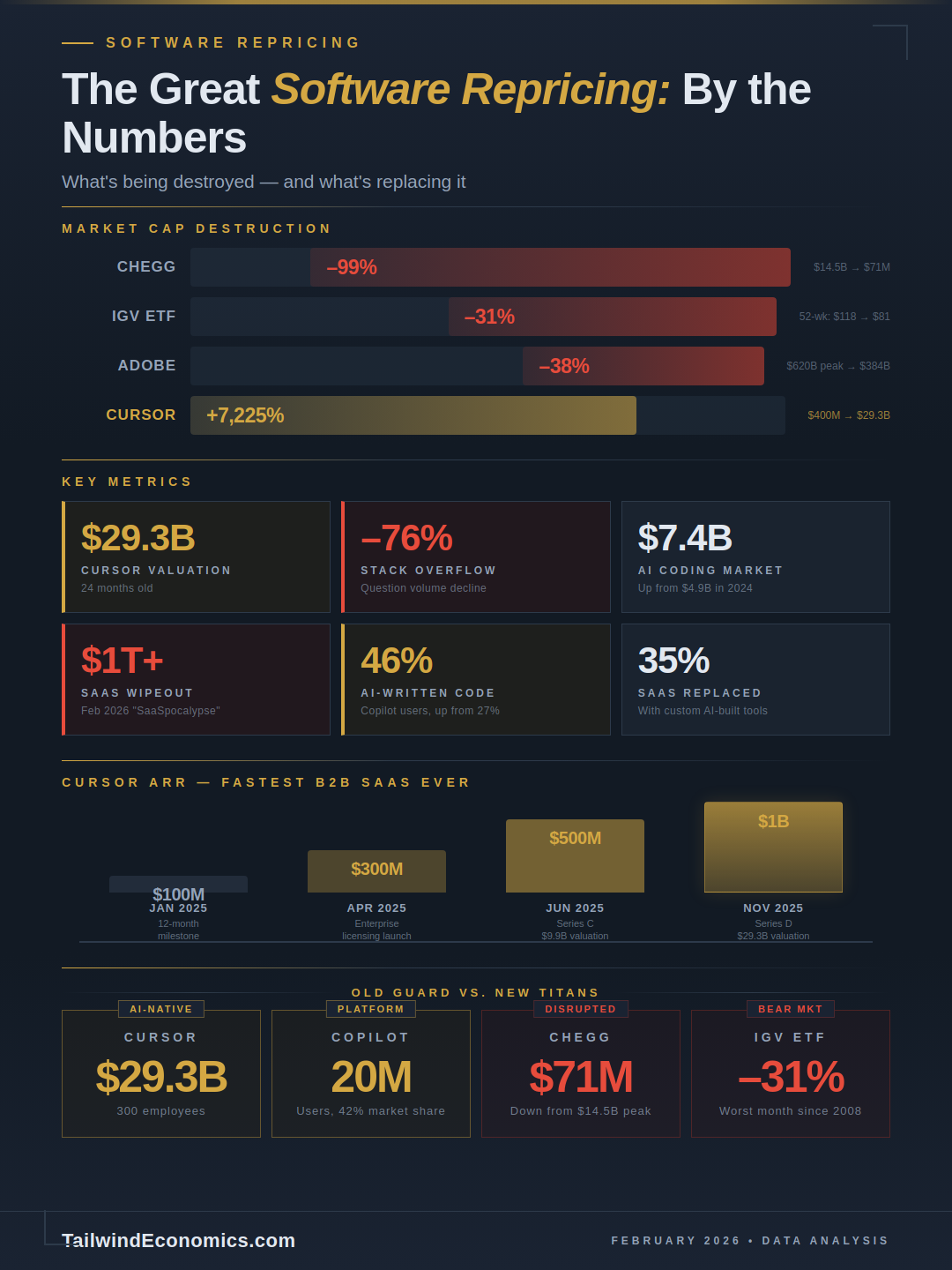

The February 2026 sell-off accelerated the downturn dramatically. The iShares Expanded Tech-Software Sector ETF (IGV) fell roughly 30% from its September 2025 peak Investing.com of $117.99 to approximately $80–82 by mid-February 2026, Ai2 vastly underperforming the broader Nasdaq 100 (flat over the same period) and the semiconductor sector (up ~30%). Investing.com Goldman Sachs noted the divergence between IGV and the broader tech index XLK reached nearly four standard deviations from the historical norm Investing.com — a statistical extreme suggesting either massive overreaction or genuine structural repricing. Investing.com

The software sector's P/E ratio collapsed from 51x to 27x in roughly twelve months, according to Goldman Sachs data. Software is no longer the most expensive sector in U.S. equities — media, autos, semiconductors, and capital goods now command higher multiples. Futu News Goldman's strategists introduced the "HALO effect" framework — Heavy Assets, Low Obsolescence — to explain why markets now reward capital-intensive businesses with physical infrastructure over capital-light software companies perceived as vulnerable to AI displacement. IndexBox

| Metric | 2021 Peak | Early 2026 | Decline |

|---|---|---|---|

| Public SaaS median EV/Revenue | 18–21x | 5–7x | ~65–75% |

| BVP Cloud Index median | ~18.4x | ~6.3x | ~66% |

| Meritech 90th percentile | 52.3x | ~13.7x | ~74% |

| Private Cloud 100 average | 34x | 20x | ~41% |

| Software sector P/E | 51x | 27x | ~47% |

| IGV from Sep 2025 peak | $117.99 | ~$80–82 | ~30% |

AI's body count: companies already disrupted

The damage is not hypothetical. Several companies have already suffered devastating, measurable impacts from AI competition.

Chegg stands as the most dramatic casualty. The education technology company's stock plummeted 48.4% in a single day CGAA on May 2, 2023, when management warned that ChatGPT was decimating its homework-help business. The decline continued relentlessly: from an all-time high of $113.51 in February 2021, shares fell below $1 by April 2025, triggering an NYSE delisting warning. Total market capitalization destruction exceeded $14.5 billion — a 99% wipeout. CNBC Non-subscriber traffic to chegg.com fell 49% year-over-year by January 2025, and organic keyword volume shrank from 11.1 million to 3.5 million (a 68% collapse). Substack The company laid off 45% of its workforce (388 employees) Rolling Out in October 2025 and filed a lawsuit against Google, arguing AI search summaries had destroyed its traffic. The Washington Post

Stack Overflow illustrates how AI can erase fifteen years of community-driven growth nearly overnight. Monthly questions posted plunged from 108,563 at ChatGPT's launch to just 25,566 by December 2024 — a 76.5% decline. Allstacks Daily active users dropped 47% between April 2024 and April 2025. Medium Prosus acquired Stack Overflow for $1.8 billion in June 2021, just before the steepest decline began PPC Land — an acquisition that now appears significantly overvalued. The company cut 28% of staff in October 2023. Allstacks Paradoxically, Stack Overflow's revenue grew to $125 million in 2024 through enterprise products and data licensing to the very AI companies destroying its consumer platform. FinalRoundAI

Adobe saw its market capitalization fall from approximately $350 billion to roughly $107 billion — a loss exceeding $240 billion — as investors priced in the threat of AI-powered design and content creation tools. Piper Sandler and Oppenheimer both downgraded the stock on AI fears. Salesforce, despite posting solid fundamentals Ai2 ($41.5 billion in FY2026 revenue, 10% growth), saw its stock decline 40%+ over twelve months as analysts warned of "seat compression" — the theory that if 10 AI agents do the work of 100 sales representatives, enterprises need 10 Salesforce seats, not 100. Ai2

Jasper AI offered a cautionary tale from within the AI ecosystem itself. The "thin wrapper on OpenAI's API" saw revenue collapse 54% from $120 million in 2023 to $55 million in 2024 Electro IQ after ChatGPT provided free competition for its core writing features. Both co-founders stepped down. Contrary Research Other casualties include UiPath (stock down 50% in 2024 as generative AI threatened its robotic process automation business), The Motley Fool Duolingo (shares down ~40% from May 2025 highs on AI translation fears), Substack and Fiverr (workforce reduced 30% as freelance tasks migrated to AI). Programs

The vibe coding revolution and the tools powering it

A new category of AI-powered development tools is enabling what Andrej Karpathy (OpenAI co-founder) coined "vibe coding" in February 2025 Natively — a term that became Collins English Dictionary's Word of the Year. Wikipedia These tools allow non-developers and small teams to build functional software through natural language, fundamentally challenging the traditional buy-versus-build calculation for businesses.

Cursor (by Anysphere) has become the fastest-growing SaaS company in history. Its revenue trajectory is extraordinary: $1 million ARR in 2023 → $100 million in 2024 → $500 million by May 2025 Artezio → $1 billion ARR by November 2025. With just ~300 employees, CNBC the company achieved a revenue-per-employee ratio exceeding $1.67 million. TapTwice Digital Its valuation soared from $400 million (August 2024) to $29.3 billion (November 2025), CNBC and it now commands roughly 18% of the AI coding assistant market. CB Insights

GitHub Copilot dominates with 42% market share Quantumrun and over 20 million users as of July 2025 AI Funding TrackerTechCrunch (up 400% year-over-year). Allstacks It has surpassed $2 billion ARR, and 90% of Fortune 100 companies have adopted it. Google Copilot now writes 46% of the average user's code, NetcorpsoftwaredevelopmentQuantumrun up from 27% at its 2022 launch. Allstacks Replit pivoted in January 2025 to target non-technical knowledge workers — "one billion new software creators" — and saw revenue explode from $16 million (December 2024) to an estimated $253 million ARR (October 2025). Readthesignal36Kr Notably, 58% of business builders on Replit are not engineers. Index.dev Lovable, a Swedish startup, reached $120 million ARR in roughly eight months MediumSacra — potentially the fastest European startup growth ever recorded.

The aggregate market is substantial and expanding rapidly. CB Insights estimates the AI coding agents and copilots market at $4 billion, with the top three players (GitHub Copilot, Claude Code, Cursor) each surpassing $1 billion ARR. CB Insights Mordor Intelligence sizes the broader AI code tools market at $7.37 billion in 2025, Quantumrun projected to reach $23.97 billion by 2030 at a 26.6% CAGR. Mordor Intelligence

The productivity evidence, however, is more nuanced than vendor claims suggest. The most rigorous independent study — a randomized controlled trial by METR involving 16 experienced open-source developers completing 246 tasks — found that developers using AI tools (Cursor Pro with Claude 3.5 Sonnet) were actually 19% slower, despite believing they were 20% faster. METR A DX Research survey of 121,000 developers found aggregate productivity gains "haven't budged past 10%" at scale, ShiftMag and a Faros AI study of 10,000+ developers found that while AI users completed 21% more tasks, PR review time ballooned 91%. Index.dev CodeRabbit found AI co-authored code contained 1.7x more major issues and 2.74x higher security vulnerabilities than human-written code. Wikipedia

The great capital rotation: VCs abandon SaaS for AI

The venture capital landscape has undergone a seismic reallocation. AI's share of global VC funding surged from approximately 18% ($55.6 billion) in 2023 to 33% ($100+ billion) in 2024 to nearly 50% ($202.3 billion) in 2025, VC Cafe according to Crunchbase. OpenAI and Anthropic alone captured 14% of all global venture investment in 2025. Foundation model companies raised $80 billion in 2025, more than doubling from $31 billion in 2024.

The concentration is extreme. The ten largest U.S. AI funding rounds in 2025 collectively raised roughly $84 billion: OpenAI ($40B), Anthropic ($13B), Databricks ($10B), xAI ($12B across rounds), Anysphere/Cursor ($2.3B), CNBC Thinking Machines Lab ($2B), SSI ($2B), and Reflection AI ($2B). Tech Funding News On Carta, 41.7% of seed capital now flows to AI companies Carta (up from 23.1% in 2020), and at Series E and beyond, AI companies capture 70.2% of all capital. DevelopmentCorporate

Traditional SaaS startups face a brutal funding environment. Carta data shows down rounds exceeded 20% of all new venture rounds in seven of eight quarters from Q2 2023 through Q1 2025. Carta The seed-to-Series A graduation rate for SaaS companies collapsed from 37% in 2020 to just 12% by H1 2022. In 2024, 966 startups shut down (a 25.6% increase from 2023), with enterprise SaaS companies comprising 32% of shutdowns. TechCrunch Private SaaS M&A transaction multiples hit a decade low of 2.9x EV/Revenue in 2024, Substack recovering only modestly to 3.8x in 2025. Aventis

Every major VC firm has pivoted decisively. Andreessen Horowitz plans to raise a record $20 billion fund specifically for AI — the largest VC fund ever excluding SoftBank's Vision Funds. AI investments now exceed 40% of a16z's portfolio. Silicon Valley BankAI Funding Tracker Bessemer Venture Partners explicitly frames vertical AI as a "10x larger opportunity" than vertical SaaS because it targets the 13% of U.S. GDP spent on business labor rather than the 1% spent on IT. VC Cafe Tiger Global, which led 212 venture rounds in 2021, completed just 9 new private investments in 2025 CNBC after suffering $23 billion in portfolio markdowns. PYMNTS Even Tiger warned that AI "valuations are elevated and sometimes unsupported by company fundamentals" TechCrunchCNBC — a rare admission of potential bubble conditions.

How small businesses are rewriting the buy-versus-build equation

Small and medium businesses are increasingly leveraging AI to replace commercial SaaS products with custom-built alternatives. A Retool survey of 817 respondents in late 2025 found that 35% have already replaced at least one SaaS tool with a custom build, and 78% expect to build more of their own tools in 2026. Newsweek Half of these builders report saving 6+ hours per week. Newsweek AI coding assistant adoption among developers jumped from 36% in 2023 to 90% in 2025, Medium according to Accel's Globalscape report. Chargebee

The SMB software market remains large — $72.35 billion in 2025 per Mordor Intelligence — and is still growing at 6.88% CAGR. Mordor Intelligence But the composition of spending is shifting. A GTIA 2025 report found that 18% of SMBs plan to reduce tech budgets before year-end, while Gartner notes that 9% of CIO IT budgets now go merely to covering price increases on existing software CIO Dive — not new functionality. SaaStr SMB-focused SaaS companies face particularly severe churn, with monthly rates of 3–7% MRRSaver (translating to 31–58% annualized), far exceeding enterprise churn of roughly 1% monthly. HubiFi

The average mid-market company runs 130+ SaaS applications at a cost of $4.2 million annually, Context Studios per Context Studios analysis. Gartner projects that 70% of new applications will be built outside traditional IT by end of 2025, and 25% of Y Combinator's Winter 2025 batch had codebases that were 95% AI-generated. Wikipedia The global vibe coding market is currently valued at $4.7 billion and projected to reach $12.3 billion by 2027 at a 38% CAGR. Digicrusader Major enterprises are already seeing results: Walmart saved 4 million developer hours using AI coding tools, and Booking.com reported saving 150,000 hours in year one at 65% adoption. Digicrusader

AI-native SaaS products, however, face their own retention challenges. Growth Unhinged's analysis of 3,500 companies found that AI-native products priced below $50/month achieved only 23% gross revenue retention — dismal by any standard. MRRSaver Products priced above $250/month performed comparably to traditional B2B SaaS, Growthunhinged suggesting that sustainable AI businesses require enterprise-grade pricing and stickiness.

Economic frameworks illuminate the structural shift

Several established economic theories help explain the current disruption.

Schumpeter's creative destruction maps directly onto the current moment. ScienceDirect A Rock & Turner analysis identified five software moats under attack (learned interface, custom workflow logic, talent scarcity, public data access, bundling) and five resilient moats (proprietary data, regulatory/compliance lock-in, network effects, transaction embedding, system of record). Substack The framework explains why the market is repricing selectively rather than uniformly: companies whose value derived primarily from interface complexity or workflow scaffolding face existential threats, while those with genuine structural scarcity retain defensibility. Substack

Christensen's disruptive innovation theory applies with textbook precision. The Christensen Institute itself noted that AI coding tools and assistants are following the classic pattern: Christenseninstitute starting with low-end tasks (basic code generation, simple content creation), being dismissed by incumbents focused on their most profitable enterprise customers, and steadily improving to move upmarket. Christenseninstitute As one analyst framed it: "The first wave of AI-native products will look like toys... New products can be built from the ground up with AI-native architectures at 10–20% of the cost." Incumbents' natural response — bolting AI features onto existing products — is precisely the "sustaining innovation" response that Christensen predicted would fail against true disruption. FredpopeChristenseninstitute

The Solow Productivity Paradox presents a fascinating tension. A February 2026 Fortune article cited an NBER study of 6,000 executives in which nearly 90% said AI had no impact on employment or productivity over three years. Yahoo Finance Apollo Chief Economist Torsten Slok observed that "AI is everywhere except in the incoming macroeconomic data." Yahoo Finance Nobel laureate Daron Acemoglu projected only a 0.5% productivity increase over the next decade from AI. Yahoo Finance Yet the Federal Reserve Bank of St. Louis found a 1.9% increase in excess cumulative productivity since ChatGPT's launch. Fortune +2 This paradox — AI visibly transforming individual companies while barely registering in aggregate statistics — mirrors the original Solow observation about computers in the 1980s, which took over a decade to resolve. Duperrin

Perhaps most consequentially, AI is inverting the zero-marginal-cost economics that made SaaS so lucrative. Traditional SaaS enjoyed 80–90% gross margins because each additional user cost nearly nothing to serve. Apollo Global Management AI-powered products face significant inference costs per interaction, Getmonetizely compressing margins to 40–60%. Medium As Amanda Huang of Bain Capital Ventures noted: "For the first time in SaaS history, the marginal cost of adding a user is not close to zero." Blockworks Simultaneously, AI is driving the cost of building software toward zero Getmonetizely — creating an asymmetry where software is cheap to create but expensive to run with AI features.

Why the bull case for software isn't dead

Despite the carnage, credible counterarguments suggest the sell-off has been indiscriminate.

Gartner projects software spending will grow 14.7% to more than $1.4 trillion in 2026 SaaStrFinancialContent — representing roughly $180 billion in net new spending, "nearly the entire software market from 15 years ago showing up as incremental spend in a single year," as SaaStr noted. SaaStr Menlo Ventures found companies spent $37 billion on generative AI in 2025 (up 3.2x from $11.5 billion in 2024), with the application layer capturing more than half of enterprise AI spend. Menlo Ventures West Monroe surveys show more than 90% of executives expect AI adoption to increase technology budgets. CIO Dive

Several large software companies are demonstrating that AI can be an accelerant rather than a threat. ServiceNow posted 21% revenue growth in Q4 FY2025, guided subscription revenue to $15.5–15.6 billion for 2026, Futurum Group and targets $1 billion in AI annual contract value for FY2026 Futurum GroupFinancialContent — all while maintaining a 98% renewal rate. Futurum Group Salesforce's Agentforce platform surged to $540 million ARR (up 330%), The Motley Fool demonstrating that consumption-based AI pricing can create new revenue streams alongside traditional seats.

Apollo Global Management published a particularly compelling analysis in February 2026, arguing: "This repricing has not been driven by collapsing demand. Enterprise software spending remains resilient, and recent earnings have largely met consensus expectations." Apollo Global Management Apollo drew a historical parallel to BlackBerry — the iPhone launched in 2007, but BlackBerry's profits didn't peak until 2011, and the company didn't exit smartphones until 2016. The transition unfolded over nearly a decade, Apollo Global Management suggesting markets may be pricing in disruption far faster than it will actually materialize.

Bank of America analyst Vivek Arya identified a logical inconsistency in the bear thesis: the market was simultaneously pricing in both scenarios — that AI capex would collapse (implying AI is overhyped) and that AI would destroy all software value (implying AI is incredibly powerful). Both cannot be true simultaneously. Ai2 +2 T. Rowe Price emphasized that software is "deeply embedded, costly to replace, and requires maintenance and updates" T. Rowe Price — enterprises with multiyear contracts, compliance requirements, and thousands of hidden workflow dependencies cannot simply rip and replace with AI overnight. Real Investment AdviceT. Rowe Price

Bifurcation, not extinction

The data points toward a market undergoing radical bifurcation rather than wholesale destruction. Goldman Sachs published research identifying 41 software companies AI will "incinerate" and 26 it will spare. Victaurs The Software Equity Group's survey found 64% of SaaS CEOs believe AI is already lowering barriers to entry in their markets. Softwareequity Gartner predicts that by 2030, 35% of point-product SaaS tools will be replaced by AI agents — but this implies 65% survive in some form. Intellectia.AI

The emerging framework distinguishes between software as interface (vulnerable) and software as infrastructure (resilient). Companies whose primary value was aggregating and presenting information — homework help, Q&A forums, basic content creation, simple workflow automation — are being disintermediated. Companies whose value lies in proprietary data, regulatory compliance, deep enterprise integrations, and system-of-record status retain formidable moats. Real Investment Advice +5 Equal Ventures' analysis of the BVP Cloud Index found that platform companies trade at 8.2x EV/Revenue versus 3.9x for traditional SaaS — a 2x premium reflecting this exact distinction. Medium

Three forces will determine the pace and depth of disruption going forward. First, the Solow Paradox resolution timeline — if AI productivity gains remain statistically invisible for years, the urgency to replace enterprise software diminishes. Second, the sustainability of AI economics — if inference costs don't decline fast enough, AI-native products may struggle to achieve the margin profiles that justified SaaS valuations. Third, and perhaps most importantly, whether vibe coding scales beyond prototypes into mission-critical enterprise software — the 45% failure rate on security tests Digicrusader and 1.7x increase in major code issues Wikipedia suggest significant quality barriers remain. The software industry isn't dying. It is being repriced for a world where code is abundant, interfaces are ephemeral, and the only durable value lies in data, trust, and deep operational embedding.

Questions:

Q: Why are SaaS and software stock valuations declining in 2025 and 2026? A: Software valuations have compressed 65–75% from 2021 highs due to a convergence of rising interest rates, slowing growth, and the structural threat of AI commoditizing core SaaS functionality. The February 2026 "SaaSpocalypse" erased over $1 trillion in market cap after Anthropic's Claude Cowork launch demonstrated AI could replace entire software workflows. Goldman Sachs noted the software sector's P/E ratio collapsed from 51x to 27x in roughly twelve months.

Q: Can small businesses use AI to build their own software instead of buying SaaS? A: Yes, and it's already happening at scale. A Retool survey found 35% of companies have replaced at least one SaaS tool with a custom AI-built alternative, and 78% plan to build more in 2026. Tools like Cursor ($29.3 billion valuation), Replit (58% of its business builders are non-engineers), and GitHub Copilot (20 million users) now enable functional app development through natural language prompts — a practice called "vibe coding." However, AI-generated code carries 1.7x more major issues and 2.74x higher security vulnerabilities than human-written code, creating real quality tradeoffs.

Q: Which software companies are most at risk from AI disruption? A: Companies whose primary value lies in aggregating and presenting information face the highest risk. Chegg lost 99% of its market cap ($14.5 billion) after ChatGPT replaced its homework-help service. Stack Overflow saw monthly questions decline 76.5% post-ChatGPT. Adobe lost over $240 billion in market value on AI design tool fears. Goldman Sachs identified 41 software companies AI will likely "incinerate" versus 26 it will spare — the dividing line is whether value comes from interface layers (vulnerable) or proprietary data, compliance requirements, and deep enterprise integrations (resilient).

Q: Is the SaaS business model dead or will software valuations recover? A: The SaaS model is being restructured, not eliminated. Gartner projects $1.4 trillion in software spending for 2026 (up 14.7%), and companies like ServiceNow (21% revenue growth, 98% renewal rate) and Salesforce ($540 million in AI-driven Agentforce ARR) demonstrate that AI can accelerate incumbent growth. Apollo Global Management compared the current moment to BlackBerry after the iPhone — the transition took nearly a decade to fully play out. Platform companies with system-of-record status trade at 8.2x EV/Revenue versus 3.9x for traditional SaaS, suggesting markets are rewarding defensibility rather than abandoning software entirely.