Private equity sits at $4.7 trillion in global buyout assets, directly employs 13.3 million American workers, and generated an estimated 7% of U.S. GDP in 2024. Yet PE-backed companies defaulted at 17% between January 2022 and August 2024 — twice the rate of non-PE firms. Steward Health Care's collapse killed patients. Red Lobster and TGI Fridays filed bankruptcy after sale-leasebacks stripped them of their own real estate. The core tension in private equity economics isn't whether the model works — it's for whom.

Why PE Deal Volume Hit $904 Billion in 2025 While Distributions Stayed Near Crisis Lows

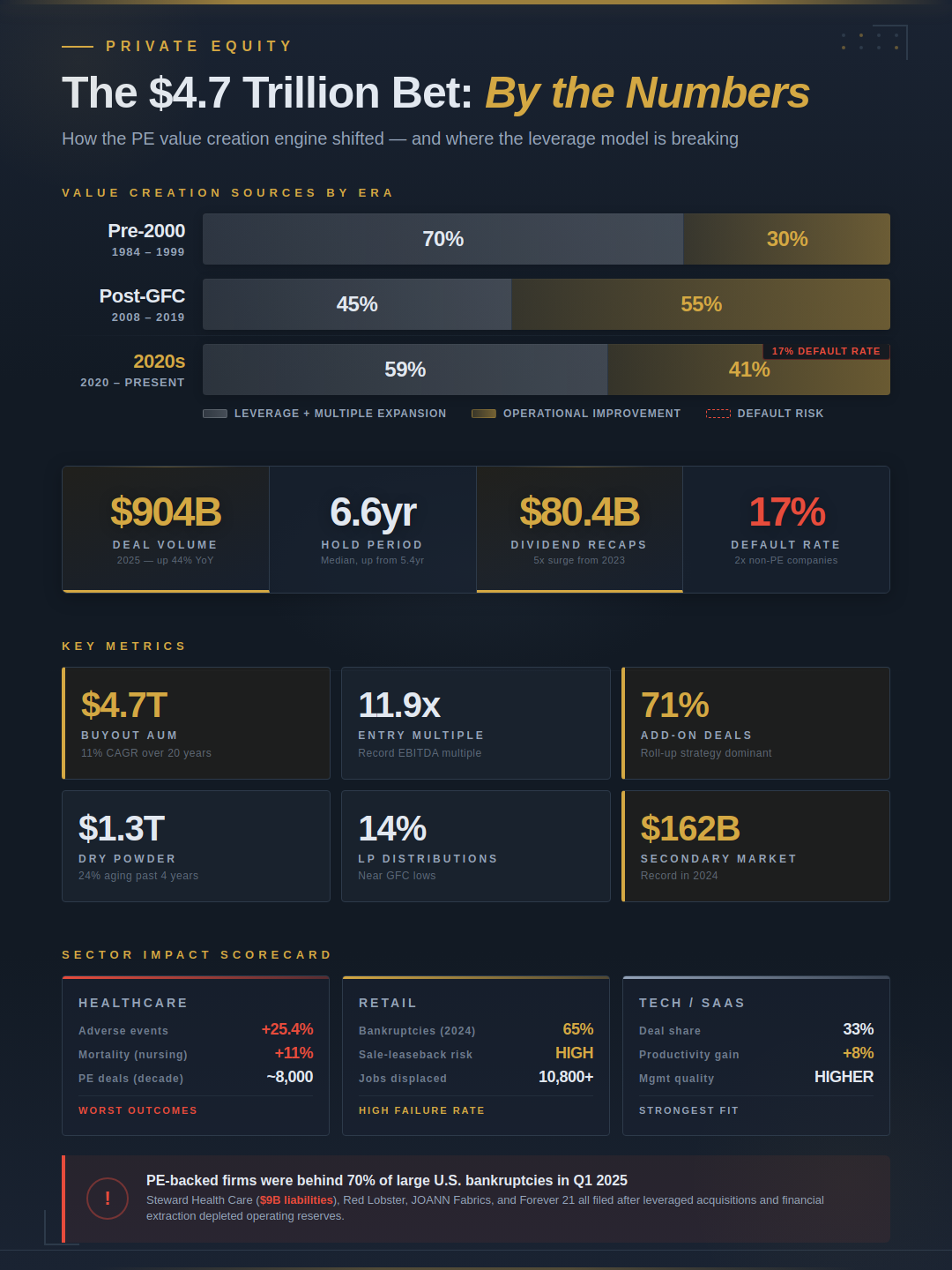

The industry's headline numbers look impressive. Global buyout deal value surged 44% to $904 billion in 2025, fueled by megadeals like Electronic Arts' $56.6 billion take-private — the largest LBO in history. Dry powder stands at roughly $1.3 trillion, with 24% of that capital aging beyond four years and creating intense deployment pressure.

But the exit side tells a different story. Distributions to limited partners remain stuck near Global Financial Crisis lows — just 14% of net asset value in 2025. An estimated 52% of portfolio companies have been held four-plus years. The median holding period stretched to 6.6 years, well above the historical average.

This backlog explains the explosion in alternative liquidity: the secondary market hit a record $162 billion in 2024, with GP-led continuation vehicles making up nearly half. PE firms are increasingly selling portfolio companies to themselves rather than finding real buyers — a dynamic that should give any allocator pause.

How PE Firms Engineer Returns: From 70% Leverage to 41% Operational Improvement

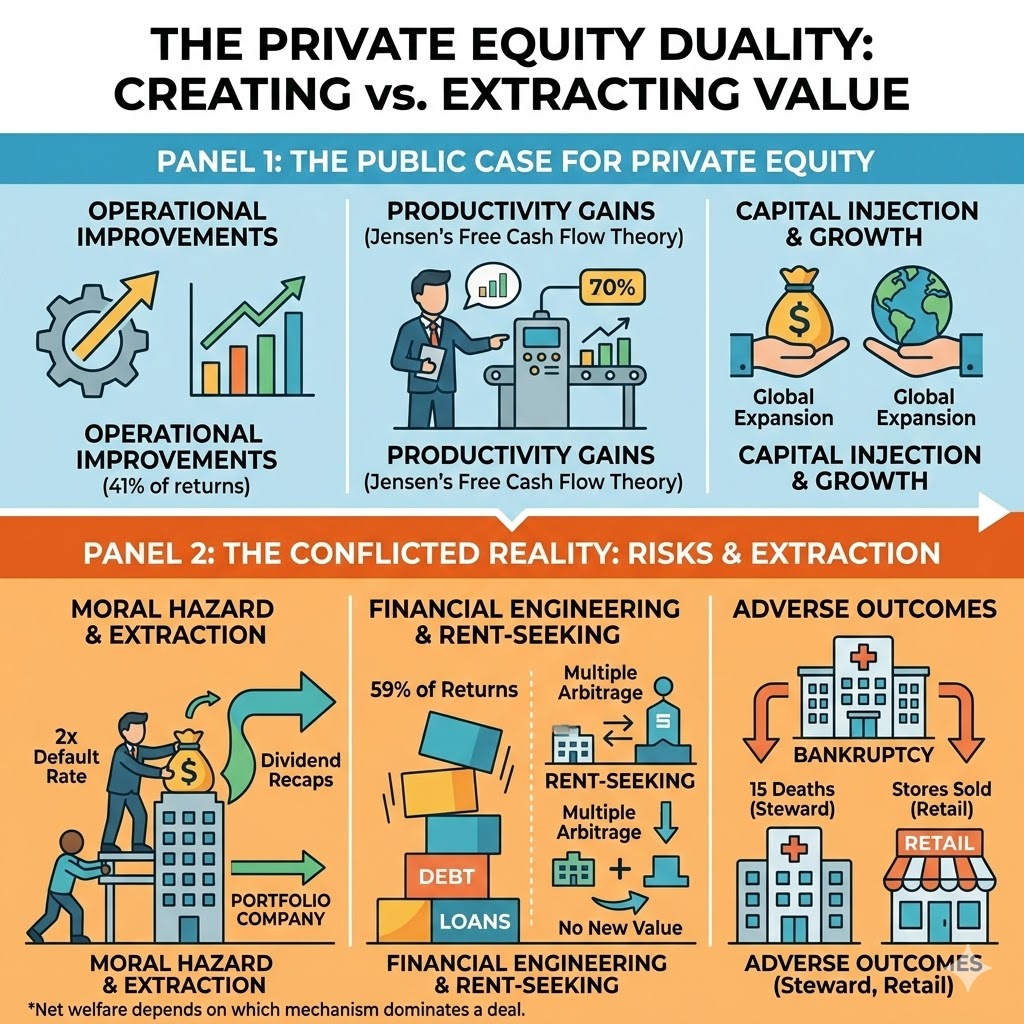

The theoretical case for PE rests on Jensen's free cash flow hypothesis — the idea that managers of cash-rich public companies waste capital on empire-building and perquisites. Concentrated PE ownership, high leverage that forces cash discipline, and active board governance solve this principal-agent problem. The empirical question is whether the cure is worse than the disease.

A comprehensive analysis of 2,951 deals from 1984-2018 reveals a dramatic shift. Before 2000, financial leverage contributed roughly 70% of total value creation. By the post-2008 era, leverage's share fell to about 25%. McKinsey's analysis of 2010-2022 deals finds leverage and multiple expansion still account for 59% of returns, with the remaining 41% from genuine operational improvement.

The financial extraction toolkit remains potent. Dividend recapitalizations — where portfolio companies take on debt to pay PE owners — surged five-fold to $80.4 billion in 2024. Add-on acquisitions have become the primary growth engine: by 2020, 71% of U.S. PE deals were add-ons. The strategy exploits multiple arbitrage — buy small companies at 4-6x EBITDA, bolt them onto a platform valued at 8-10x, and pocket the spread without creating a dollar of new value.

PE-Backed Companies Default at Twice the Rate — and the Evidence on Workers Is Mixed

The most rigorous employment research comes from Davis, Haltiwanger, et al., whose Census Bureau microdata spanning 1980-2013 shows massive variation by deal type. Public-to-private buyouts destroy jobs aggressively — employment shrinks 12-13% over two years. But private-to-private deals actually expand employment by 13-15%.

Productivity gains are robust. The same researchers document 8% total factor productivity improvements over two years. Bloom, Sadun, and Van Reenen's study of 15,000 firms confirms PE-owned companies are significantly better managed than family- or government-owned peers. Lerner, Sørensen, and Strömberg find no evidence that buyouts reduce innovation — post-LBO patents are more frequently cited and more focused.

The bankruptcy data, however, reveals the cost of leverage. PE-backed bankruptcies hit a record 110 in 2024, with PE firms behind 65% of billion-dollar U.S. bankruptcies. The pattern — leveraged acquisition, cost-cutting, dividend extraction, inability to reinvest, bankruptcy — has become a familiar cycle in retail and healthcare. This is creative destruction with a twist: the destruction is often engineered by the owners, not the market.

Healthcare and Retail: Where the Leveraged Playbook Produces the Worst Outcomes

A JAMA study of 662,095 hospitalizations found a 25.4% increase in hospital-acquired adverse events after PE acquisition. An NBER study of nursing homes documented an 11% increase in short-term mortality at PE-acquired facilities.

Steward Health Care is the defining case. Cerberus Capital Management executed a $1.25 billion sale-leaseback in 2016, extracted roughly $800 million over a decade, then watched the system collapse into bankruptcy in May 2024 with $9 billion in liabilities — five hospitals closed, at least 15 patients died, and 2,400 workers were laid off.

Retail tells a parallel story. Red Lobster filed after Golden Gate Capital's sale-leaseback forced it to pay inflated rents on properties it once owned. JOANN Fabrics filed twice before liquidating all stores. Forever 21 announced closure of all U.S. locations in March 2025. The common thread: PE owners extracted value through real estate transactions and dividend recaps, leaving the operating companies too debt-laden to invest in competitiveness.

The FTC has taken notice. Its January 2025 settlement with Welsh Carson over US Anesthesia Partners marked the first-ever antitrust challenge to a PE roll-up strategy. States are moving faster: Massachusetts passed healthcare transaction oversight legislation in January 2025 after Steward's collapse.

What PE's Shifting Economics Mean for Investors, Operators, and Policymakers in 2026

The era of easy leveraged returns is ending. Entry multiples hit record 11.9x EBITDA in North America, cheap debt is gone, and average management fees fell to an all-time low of 1.61%. Bain's 2026 report declares "12 is the new 5" — meaning deals now need substantially faster EBITDA growth because financial engineering alone can't generate target returns.

Three signals to watch:

For investors and allocators: Manager selection has never mattered more. Dispersion between top- and bottom-quartile funds exceeds 1,000 basis points. Ask hard questions about how much of a fund's historical returns came from leverage and multiple expansion versus operational improvement. If the answer is vague, the next vintage will underperform.

For operators and business owners: If a PE firm is acquiring in your industry, study the add-on playbook. With 71% of deals now being bolt-ons, your company may be a target for multiple arbitrage. Understand whether the acquirer is buying your business to grow it — or to resell it at a higher multiple.

For policymakers: The regulatory gap is real. The SEC's Private Fund Adviser Rules were vacated by the Fifth Circuit in June 2024, leaving no federal transparency requirements for a $4.7 trillion industry. The FTC's Welsh Carson settlement was a start, but state-by-state healthcare regulation is an inadequate response to a national-scale problem.

The academic evidence is clear: PE improves productivity and management quality while simultaneously elevating bankruptcy risk, depressing wages for displaced workers, and — in healthcare — worsening patient outcomes. The net welfare calculation depends on whether a roughly 3% annual return premium over public markets justifies the externalities that concentrated leverage imposes on workers, consumers, and communities.

The Economic Principles That Explain Why PE Works — and When It Doesn't

Private equity sits at the intersection of several competing economic theories. Which framework applies depends entirely on the deal structure and sector.

Agency Theory. The intellectual case for PE begins with Jensen and Meckling's principal-agent problem. Public company managers hoard cash, pursue vanity acquisitions, and resist restructuring. Jensen's free cash flow hypothesis argues that debt disciplines this behavior — forcing managers to generate cash rather than waste it. PE operationalizes this theory through concentrated ownership, high leverage, and active governance. The 8% productivity gains documented across PE-owned firms suggest the mechanism works.

The Modigliani-Miller Leverage Paradox. The Modigliani-Miller theorem holds that capital structure is irrelevant to firm value in perfect markets. PE exploits every departure from this ideal — particularly the tax shield on interest payments, which subsidizes leverage by reducing taxable income. When rates were near zero from 2009-2021, this subsidy was enormous. Now that borrowing costs have normalized, the tax shield advantage has shrunk, helping explain why PE returns are compressing.

Moral Hazard. The most troubling dynamic in PE is moral hazard — the distortion when one party bears risk while another captures reward. Dividend recapitalizations are the clearest example: PE owners extract returns before the investment thesis plays out. If the company collapses, creditors and employees absorb losses while the fund keeps its dividends. This asymmetric payoff structure explains why PE-backed firms default at twice the rate of non-PE companies — the ownership model incentivizes risk-taking because downside is externalized.

Rent-Seeking vs. Value Creation. Economists distinguish between productive entrepreneurship and rent-seeking — creating new wealth versus redistributing existing wealth. PE's add-on strategy sits uncomfortably on this line. When a platform acquires a competitor at 5x EBITDA and the combined entity is valued at 10x, multiple arbitrage generates paper value without producing a new product or efficiency gain. The FTC's Welsh Carson settlement explicitly targeted this dynamic as anticompetitive consolidation.

The Market for Corporate Control. Henry Manne's theory provides PE's strongest defense: poorly managed companies should be acquired, and the takeover threat disciplines all managers. Bloom, Sadun, and Van Reenen confirm PE-owned firms exhibit measurably higher management quality across 15,000 companies. But Manne's theory assumes acquirers aim to improve operations — not strip assets. When the playbook is sale-leaseback, dividend recap, and exit, the market for corporate control becomes a market for financial extraction.

The core insight: PE's impact depends on which mechanism dominates. When agency theory and corporate control drive the deal, outcomes are positive. When moral hazard and rent-seeking dominate, the same ownership structure produces bankruptcy, job destruction, and patient harm. The theory doesn't predict one outcome — the deal structure determines which theory governs.

Questions:

Q: How does private equity make money from acquired companies? A: PE firms generate returns through three primary mechanisms: financial leverage (using debt to amplify equity returns), operational improvement (cutting costs and growing revenue), and multiple arbitrage (buying at lower valuation multiples and selling higher). Leverage and multiple expansion still account for roughly 59% of returns, per McKinsey's 2026 analysis, with 41% from operational gains.

Q: Do private equity buyouts cause layoffs? A: It depends on the deal type. Research from Davis, Haltiwanger, et al. using Census data shows public-to-private buyouts cut employment 12-13% over two years, but private-to-private deals actually expand jobs by 13-15%. Across all deal types, net job losses are modest (1-3%), though gross job reallocation — simultaneous creation and destruction — exceeds controls by 13-14 percentage points.

Q: What is the average return on private equity investments? A: The Cambridge Associates U.S. PE Index returned 8.1% net in 2024, with a 10-year horizon IRR of 15.25%. Hamilton Lane data shows $1 invested in PE in 2015 grew to $3.96 by 2024, versus $3.51 for the S&P 500 — but the outperformance gap has narrowed considerably, and post-2018 vintages show MOICs in the 1.3-1.6x range.

Q: Why do so many private equity-backed companies go bankrupt? A: High leverage is the primary driver. PE-backed companies defaulted at 17% between 2022-2024 — twice the rate of non-PE firms, per Moody's. The typical failure pattern involves leveraged acquisition, cost-cutting that degrades competitiveness, dividend recapitalizations that add more debt, and eventual inability to service obligations — particularly when interest rates rise or consumer demand shifts.

Q: What economic theories explain how private equity creates and destroys value? A: Five frameworks are central: Jensen's free cash flow hypothesis (debt disciplines wasteful managers), agency theory (concentrated ownership aligns incentives), Modigliani-Miller (leverage exploits tax shields but creates fragility), moral hazard (PE owners externalize downside risk via dividend recaps while capturing upside), and rent-seeking theory (multiple arbitrage and roll-ups can redistribute value rather than create it). Which framework dominates depends on the deal structure and sector.

Sources: Bain & Company Global PE Report 2026 (Feb 2026), McKinsey Global Private Markets Report 2026 (Feb 2026), Cambridge Associates US PE/VC Benchmark (2024), Davis et al. — Private Equity, Jobs, and Productivity (NBER) (2014), JAMA — Hospital Adverse Events After PE Acquisition (Dec 2023), Gupta et al. — PE Investment in Nursing Homes (NBER) (2021), PE Stakeholder Project Bankruptcy Tracker (2025), Lazard Secondary Market Report (2024), FTC Welsh Carson Settlement (Jan 2025), CAIS — Drivers of PE Value Creation (2024)