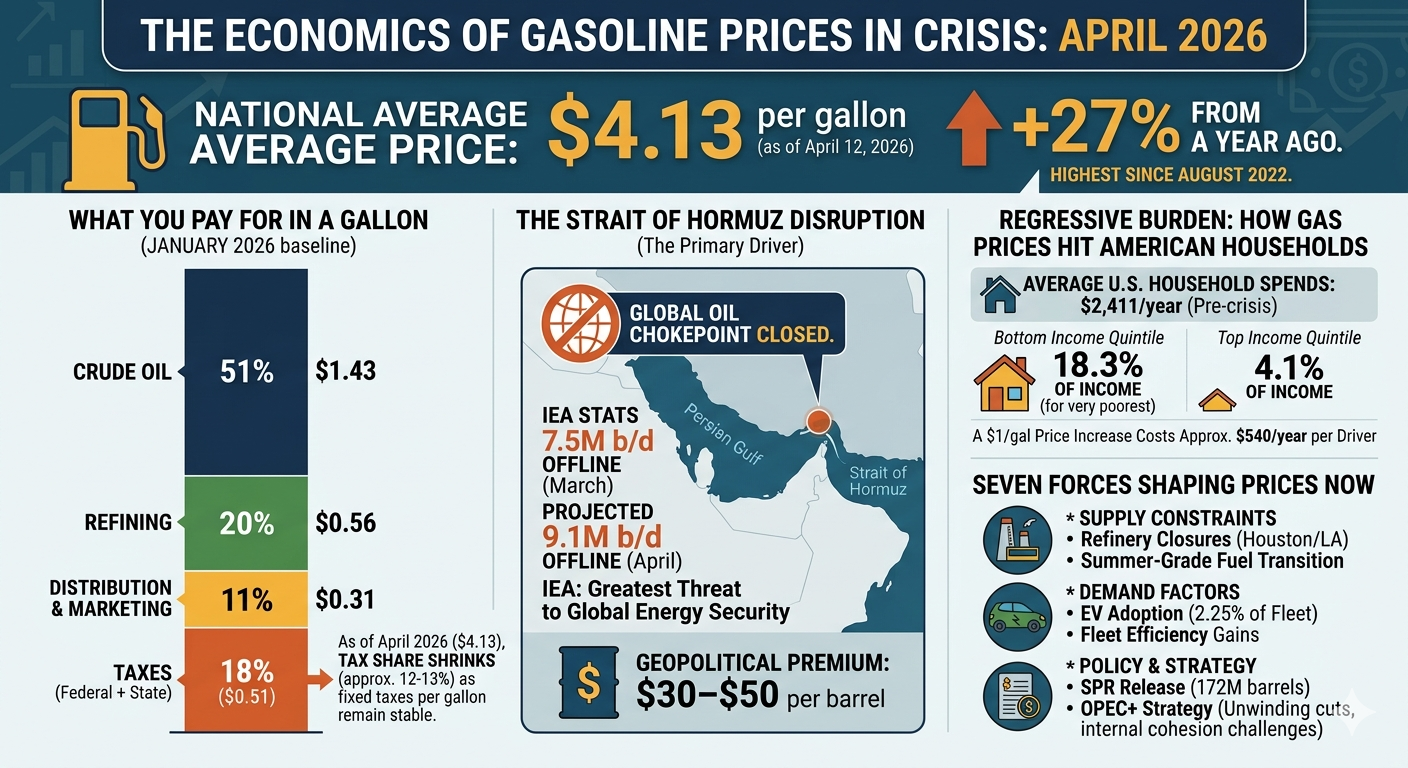

American drivers are paying $4.13 per gallon for regular gasoline as of April 12, 2026 — up 27% from a year ago and the highest since August 2022 — driven primarily by the largest oil supply disruption in modern history. The U.S.-Israeli military campaign against Iran and the subsequent closure of the Strait of Hormuz have injected a $30–$50 per barrel geopolitical premium into crude oil, transforming what was shaping up to be a year of sub-$3 gasoline into a potential repeat of the 2022 price shock. For the average American household spending $2,411 annually on fuel, this surge functions as a deeply regressive tax — consuming nearly one-fifth of the poorest households' income while barely registering for the wealthiest. Understanding why gasoline costs what it does requires examining the interplay of crude oil markets, refinery economics, OPEC+ cartel strategy, and the unique demand characteristics that make gasoline one of the most economically significant commodities in daily life.

From $2.81 to $4.13 in three months

The speed of the 2026 gasoline price surge has been extraordinary. On January 8, AAA recorded a national average of $2.81 per gallon — the lowest since March 2021. By February 26, prices had barely moved, sitting at $2.98. Then the Iran conflict erupted on February 28, and everything changed. Gasoline jumped 27 cents in a single week to $3.25 by March 5, then another 35 cents to $3.60 by March 12. On April 2, the national average crossed $4.00 for the first time since August 2022. The EIA's April Short-Term Energy Outlook forecasts prices peaking around $4.30 in April before averaging $3.70 for the full year — a dramatic revision from its pre-conflict forecast of $2.90–$3.00.

State-level variation remains stark. California leads at $5.89 per gallon, driven by its unique fuel blend requirements, Low Carbon Fuel Standard surcharges (~17 cents/gallon), and the highest state gas taxes in the nation. Hawaii follows at $5.65 and Washington at $5.39. At the other extreme, Oklahoma drivers pay just $3.45 per gallon, with Kansas ($3.49), Nebraska ($3.61), and North Dakota ($3.61) close behind. The $2.44 spread between California and Oklahoma reflects the compounding effects of state taxes, fuel specifications, refinery proximity, and local market competition.

For historical context, the all-time national average peaked at $5.02 per gallon on June 14, 2022, during the post-Ukraine invasion price shock. The 2022 annual average of $3.95 remains the highest on record. Current prices, while elevated, remain roughly 18% below that peak — though the trajectory has rattled markets and consumers alike.

What you actually pay for in a gallon of gas

The EIA's most recent composition breakdown (January 2026, when gasoline averaged $2.81) reveals the anatomy of a gallon of regular unleaded. Crude oil accounts for 51% of the retail price (~$1.43), refining costs and profits take 20% (~$0.56), distribution and marketing absorb 11% (~$0.31), and federal plus state taxes claim 18% (~$0.51). Over the prior decade, crude oil has consistently represented slightly more than half the pump price, though this share fluctuates significantly with oil market conditions.

The tax component deserves particular attention. The federal excise tax has been frozen at 18.3 cents per gallon since 1993 — eroding roughly 55% of its real value to inflation. Average state taxes add another 33.55 cents, for a combined 51.95 cents per gallon in fixed per-unit levies. Because these taxes are assessed per gallon rather than as a percentage of price, their share of the total shrinks as prices rise. At $2.81 per gallon, taxes represent 18% of the price. At today's $4.13, they represent roughly 12–13%. This means the crude oil share at current prices has likely climbed well above 55–60%, though the EIA has not yet published an updated April breakdown.

The 10-year average composition (2014–2023) tells a broadly similar story: crude oil at 52.3%, refining at 15.3%, distribution and marketing at 15.1%, and taxes at 17.3%. What shifts most dramatically across price cycles is the refining margin. Crack spreads — the difference between crude input costs and refined product prices — have widened considerably in 2026 due to reduced domestic refinery capacity and the abnormally wide Brent-WTI spread that peaked at $25 per barrel in late March, far above the typical $3–$5 range.

Crude oil markets are pricing in a war

The current price environment is dominated by one overriding reality: the Strait of Hormuz crisis. WTI crude settled around $95.50–$96.57 per barrel on April 10, while Brent traded at approximately $95.20 — both roughly 47% above year-ago levels. These prices represent a substantial pullback from the March–April peaks: Brent briefly touched $128 per barrel on April 2, and WTI exceeded $100 for the first time since 2022. A ceasefire announcement on April 8 triggered a 13% single-day crash — the steepest since 2020 — but the Strait remains effectively closed, and prices have stabilized in the mid-$90s.

The scale of disruption is historically unprecedented. The IEA estimates that 7.5 million barrels per day of production were shut in during March, rising to a projected 9.1 million barrels per day in April — a figure the IEA described as "the greatest threat to global energy security in history." For context, approximately 20 million barrels per day of oil normally transit the Strait of Hormuz, representing 20% of global petroleum consumption and 25–27% of all seaborne oil trade. Only Saudi Arabia and the UAE possess pipeline bypass capacity, estimated at 3.5–5.5 million barrels per day.

U.S. domestic production provides a partial buffer. At 13.6 million barrels per day (week ending April 3), U.S. output sits near its all-time record, though the EIA forecasts a gentle decline to 13.5 million barrels per day for 2026 and 13.3 million in 2027 — the first annual decline since 2021. The active oil rig count has fallen to 411 rigs, down 70 from a year ago and continuing a multi-year decline from 775 in January 2023. Despite this, improved well productivity has kept output near records — a testament to the shale revolution's efficiency gains but also a warning that the easy growth may be ending.

Before the Iran conflict, the global oil market was heading into significant oversupply. The IEA had projected a surplus of 3.7–3.8 million barrels per day for 2026, with global inventories having built at 1.3 million barrels per day throughout 2025, pushing total observed stocks above 8.2 billion barrels — the highest since February 2021. The conflict has violently reversed this trajectory, with the EIA now projecting an inventory draw of 5.1 million barrels per day in Q2 2026.

Middle Eastern conflicts and oil — a pattern of diminishing returns, broken spectacularly

Prior to 2026, a striking pattern had emerged in how oil markets responded to Middle Eastern geopolitical risk: each successive crisis produced a smaller and shorter-lived price impact. The October 2023 Hamas attack generated a $3–$4 per barrel risk premium that faded within weeks. Houthi Red Sea attacks beginning in November 2023 disrupted 65–70% of Red Sea shipping transits — rerouting tankers around Africa's Cape of Good Hope at 10–14 additional days per voyage — yet oil prices barely budged. The June 2025 twelve-day Israel-Iran war pushed Brent from $64 to $76, only for prices to snap back after ceasefire. Markets had learned to distinguish between geopolitical noise and actual supply disruption.

The 2026 Iran conflict shattered that complacency. When the Strait of Hormuz physically closed and 10 million barrels per day went offline, the price response was immediate and massive: WTI posted its largest weekly gain in history at 35.6%. Brent's March surge of approximately 55% exceeded even September 1990's 46% monthly gain during the Gulf War. The lesson is clear: markets can efficiently price distant geopolitical risk, but actual physical supply disruption at a critical chokepoint overwhelms all hedging and speculation.

Historical comparisons illuminate the current moment. The 1973 Arab oil embargo removed roughly 9% of global supply, quadrupling prices from $3 to $12 per barrel over five months and triggering a U.S. recession that shrank GDP by 2.5%. The 1979 Iranian Revolution cut 4.8 million barrels per day — about 7% of global output — and more than doubled prices over 12 months, fueling the stagflation that prompted the Federal Reserve to raise interest rates to 19%. The 1990 Gulf War took 4.3 million barrels per day offline and drove oil from $15 to $41 (a 173% spike), though prices collapsed almost immediately when military operations began. The 2019 Abqaiq drone attack knocked out 5.7 million barrels per day — the largest single-event disruption in volume terms — but Saudi Aramco's rapid repair response and spare capacity brought prices below pre-attack levels within two weeks.

The 2026 crisis combines the worst features of multiple predecessors: a chokepoint disruption like the hypothetical Hormuz scenarios analysts have modeled for decades, production losses exceeding any previous event, and a conflict whose resolution timeline remains deeply uncertain. Analyst estimates of the geopolitical risk premium in current prices range from $30–$50 per barrel above the fundamental baseline of approximately $55–$60 — the level banks like Goldman Sachs and JP Morgan had forecast for 2026 before the conflict.

How gas prices hit American households

The burden of gasoline costs falls with punishing asymmetry across the income spectrum. According to the 2024 BLS Consumer Expenditure Survey, the average American household spends $2,411 per year on gasoline — 3.1% of total expenditures. But this average conceals a regressive reality. The bottom income quintile (below $29,932 annually) spends $1,177 on gas — less in absolute terms, but consuming 3.4% of their total budget. ACEEE analysis paints an even starker picture: low-income households devote 13.8% of their income to gasoline, with the very poorest (below $20,800) spending 18.3%. High-income households, by contrast, spend $3,477 — nearly three times more in dollars — but just 2.3% of their budget and roughly 4.1% of income.

A useful rule of thumb: the average American driver covers approximately 13,500 miles per year in a vehicle averaging roughly 25 miles per gallon, consuming about 540 gallons annually. A $1 per gallon price increase therefore costs the typical driver $540 per year — or roughly $1,080 for a two-driver household. At the median household income of $81,604, that represents 0.66% of earnings. For a bottom-quintile household, the same increase absorbs nearly 1.8% of income. Since January 2026, the national average has risen approximately $1.30 per gallon, implying an annualized cost increase of roughly $700 per driver.

Rural households face compounded exposure. BLS data shows rural families spend approximately $500 more per year on gasoline than urban households, driven by longer commutes and fewer transportation alternatives. Drivers in Wyoming average over 21,000 miles annually; New York City residents average under 5,000. Rural households are also less likely to have access to public transit, more likely to drive older, less fuel-efficient vehicles, and less able to substitute electric vehicles or alternative transportation.

Why gas prices behave the way they do

Gasoline occupies a peculiar position in consumer economics: it is one of the most visible, frequently purchased, and psychologically salient prices in daily life, yet consumers have remarkably little ability to adjust their consumption in response to price changes. The short-run price elasticity of demand for gasoline is approximately -0.25 to -0.37, according to methodologically rigorous recent estimates from Coglianese, Davis, Kilian, and Stock. A Dallas Fed review found these modern estimates are five to twenty-five times larger than earlier studies (which had suggested elasticities as low as -0.03), but the fundamental insight holds: a 10% gasoline price increase reduces consumption by only 2.5–3.7% in the short run. The long-run elasticity is considerably higher at -0.6 to -0.84, reflecting consumers' eventual ability to purchase more efficient vehicles, relocate, or adopt alternative transportation — adjustments that take years.

This inelasticity explains why supply shocks produce outsized price movements. When OPEC+ cuts production or the Strait of Hormuz closes, even modest supply reductions require large price increases to bring supply and demand back into balance. The asymmetry works in reverse too: when supply expands, prices need to fall significantly to stimulate enough additional consumption to clear the market.

The transmission from crude oil to the pump follows its own distinctive pattern. Dallas Fed research by Chudik (2019) estimates that roughly 12% of a crude oil price change passes through to retail on the same day, approximately 50% within four weeks, and 55% in the long run. The incomplete pass-through reflects that crude oil is only one cost component — refining margins, distribution costs, and fixed per-gallon taxes dilute the percentage impact. Hamilton's rule of thumb provides a practical shortcut: a $10 per barrel change in crude oil translates to roughly 25 cents per gallon at the pump.

Perhaps the most well-documented behavioral pattern in gasoline markets is the "rockets and feathers" phenomenon — first formally documented by Robert Bacon in 1991 and extensively studied by Borenstein, Cameron, and Gilbert. Retail prices rise rapidly when crude costs increase but decline slowly when costs fall, with speed ratios reaching 3:1 to 4:1 during volatile periods. The causes include imperfect retail competition, replacement-cost pricing by stations uncertain about future wholesale prices, and asymmetric consumer search behavior — people pay closer attention when prices rise than when they fall. The practical implication is that the current crude pullback from $128 to $95 will take weeks to fully register at the pump.

On the question of speculation, academic consensus holds that fundamentals — supply and demand — are the primary drivers of oil prices. A landmark CFTC study found that price changes lead speculator positions, not the reverse, suggesting speculators are trend followers rather than trend setters. Irwin and Sanders at the University of Illinois concluded there is "no smoking gun connecting speculation to the rise in gas prices" and that expanded speculative participation likely reduces hedging costs and dampens volatility. This does not mean futures markets are irrelevant — they transmit information and expectations rapidly — but the narrative that speculators artificially inflate gas prices lacks robust empirical support.

Seven forces shaping prices right now

Beyond the dominant Iran crisis, several structural and cyclical forces are simultaneously pushing gasoline prices in different directions. On the supply-constraining side, the permanent closures of the LyondellBasell Houston refinery (263,776 barrels per day) and Phillips 66 Los Angeles refinery (138,700 barrels per day) have removed roughly 400,000 barrels per day of U.S. refining capacity — tightening the domestic supply chain and pushing refinery utilization to 92.9%. Seasonal factors are also applying upward pressure: the transition to summer-grade gasoline (with lower Reid Vapor Pressure specifications) increases production costs, and the approaching summer driving season historically adds 20–40 cents per gallon. Canadian oil tariffs of 10% — imposed in March 2025 — add an estimated 5–15 cents per gallon, though their legal status remains uncertain after a February 2026 Supreme Court ruling.

On the demand-suppressing side, EV adoption continues to erode gasoline consumption at the margins. The U.S. had approximately 6.8–7.0 million EVs on the road as of early 2026, representing about 2.25% of the total vehicle fleet. However, EV market share fell to 5.8% of new car sales in Q1 2026, down sharply from a peak of 10.5–12% in Q3 2025, after the expiration of the $7,500 federal tax credit in September 2025. Globally, EVs displaced an estimated 2.3 million barrels per day of oil demand in 2025, with the IEA projecting global gasoline demand will peak in 2026 at 27.4 million barrels per day. But in the U.S. specifically, overall fuel efficiency improvements — the on-road fleet now averages roughly 25–26 MPG — matter more than EVs at current adoption levels. U.S. gasoline consumption declined about 1% in 2025 to 8.91 million barrels per day, or 4.5% below its 2018 peak.

The Strategic Petroleum Reserve is being deployed aggressively. The Trump administration authorized a 172-million-barrel release in March — the largest single drawdown in SPR history — as part of a coordinated IEA action totaling 400 million barrels across 32 nations. SPR inventory has fallen to approximately 367 million barrels, or 51% of its 714-million-barrel capacity, down from a peak of 726.6 million barrels in 2009 and pre-2022 levels of roughly 580 million barrels. First oil deliveries began just nine days after the presidential decision. While the release has provided some market relief, crude remains above $95 — suggesting the disruption's scale exceeds what strategic reserves can fully offset.

OPEC+ is navigating its most complex moment in decades

The OPEC+ alliance holds enormous market influence, with effective production cuts totaling approximately 5.86 million barrels per day — roughly 5.7% of global demand — spread across three overlapping layers of agreements dating to 2022 and 2023. The cartel's spare production capacity, concentrated overwhelmingly in Saudi Arabia and the UAE, represents the world's primary supply buffer. Estimates range from 3.5 million barrels per day (Rystad Energy) to 5.3 million (IEA), though the EIA quietly revised its methodology in January 2026, producing estimates roughly 60% lower than traditional figures. Saudi Arabia produces about 10.1 million barrels per day against a claimed maximum capacity of 12.0–12.5 million, though recent attacks have reduced this by approximately 600,000 barrels per day.

The alliance has begun unwinding its voluntary cuts, approving 206,000 barrels per day increases for both April and May 2026 — larger than the 137,000-barrel increments used in late 2025. But the Hormuz crisis makes these decisions "partially academic," as several member states physically cannot export through their normal routes regardless of quota allocations. The deeper strategic dilemma is what happens when the conflict resolves: the IEA projects an implied oversupply of 3.8 million barrels per day once Gulf production and shipping resume, which would require careful supply management to prevent a price collapse.

Internal cohesion remains OPEC+'s Achilles' heel. Cumulative overproduction since January 2024 totals 4.779 million barrels per day across members, with Kazakhstan the worst offender (2.63 million barrels of required compensation), followed by Iraq (1.4 million) and Russia (consistently producing 200,000–500,000 barrels per day above target). Angola departed the alliance entirely in 2024 over quota disputes. The UAE has expanded capacity to 4.85 million barrels per day and is pushing for larger allocations, while a contentious maximum sustainable capacity assessment in 2026 will determine 2027 quotas — creating incentive for members to overstate their capabilities.

Saudi Arabia's role as swing producer anchors the alliance. Riyadh has maintained near-perfect compliance despite forgoing substantial revenue, producing well below its capacity to support prices. With a fiscal breakeven estimated around $80 per barrel, current prices above $95 generate comfortable surpluses. But the kingdom's willingness to shoulder disproportionate cuts indefinitely is not guaranteed, particularly if other members continue free-riding on Saudi restraint.

Why a 21-Mile Waterway Still Controls What You Pay at the Pump

The gasoline market of April 2026 illustrates a fundamental truth about energy economics: prices are set at the margin, and margins can shift violently. A global oil market that was heading into substantial oversupply just weeks ago has been transformed by the physical closure of a single 21-mile-wide waterway into the tightest supply environment in decades. The EIA's April forecast revision — from $2.90 to $3.70 per gallon for the 2026 average — represents one of the largest single-month adjustments in the agency's history.

Three insights stand out. First, the pre-2026 pattern of markets shrugging off Middle Eastern geopolitical risk was not evidence that geography no longer matters — it was evidence that markets correctly distinguish between political tension and physical supply disruption. When the Strait of Hormuz actually closed, the response was immediate and enormous. Second, structural changes are quietly reshaping gasoline demand — EV adoption, efficiency improvements, and shifting driving patterns have pushed U.S. consumption 4.5% below its 2018 peak — but these trends operate on timescales of years and decades, not the weeks and months that geopolitical crises unfold over. Third, the regressive burden of gasoline prices remains one of the most consequential distributional issues in the U.S. economy: a household earning $20,000 devotes nearly a fifth of its income to fuel, while a household earning $150,000 barely notices the cost. Every dollar added to the price of a gallon extracts $540 per year from the average driver — a transfer that falls hardest on those least able to absorb it.